FINE WINE INVESTMENT MARKET DYNAMICS IN 2026

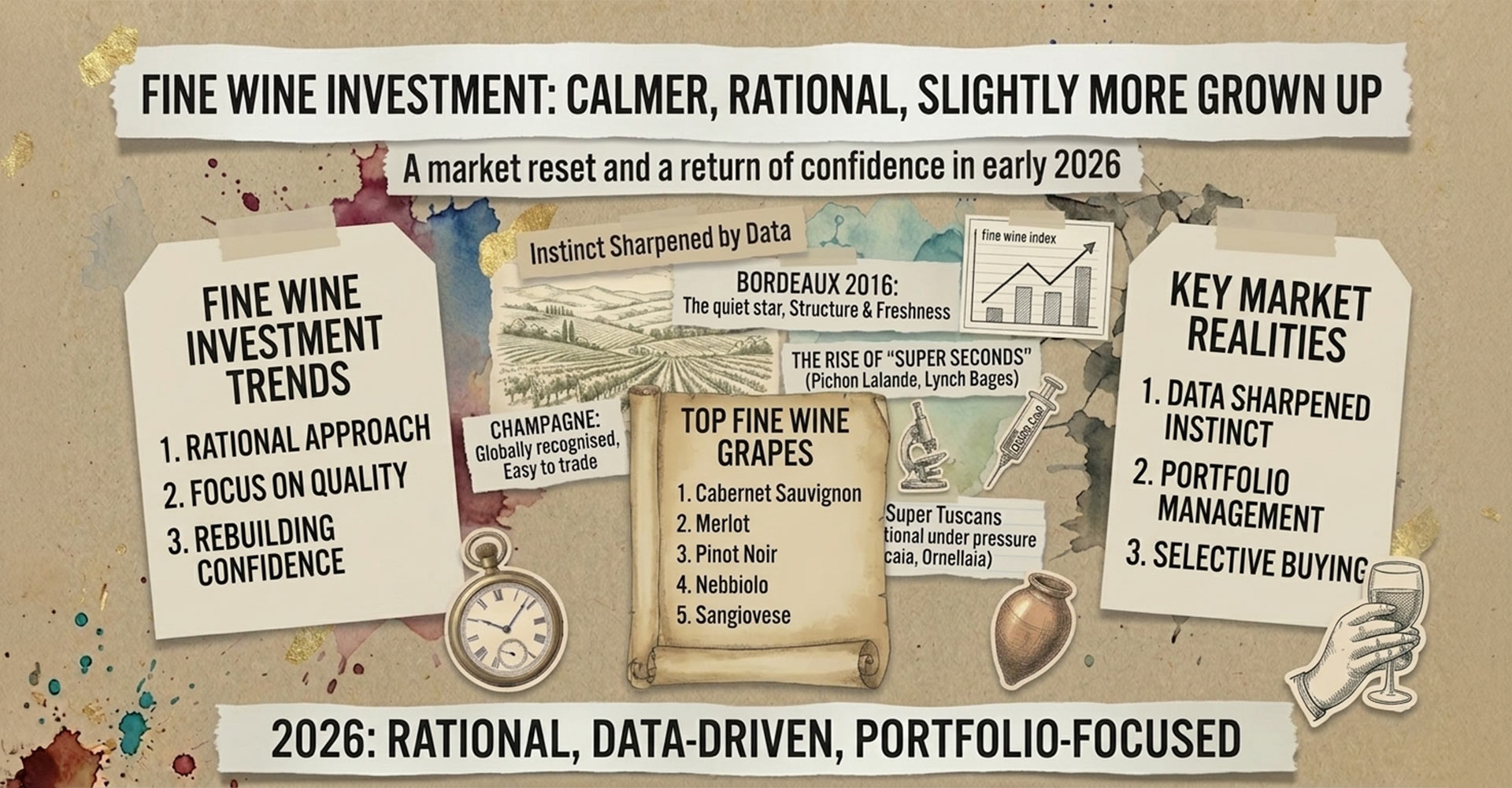

The fine wine investment market in 2026 is characterized by stabilization after a correction, selective regional performance, and evolving consumer and trading behaviors.

- Market has stopped falling, with top-tier wines leading recovery and mid-tier regions adjusting.

- Fine wine shows low correlation with equities, providing relative stability amid global market volatility.

- Key regions: Bordeaux 2016 vintage gains attention; Super Seconds offer quality at discounts; Champagne leads early recovery; Burgundy and Italy show mixed performance.

- Shift towards premium consumption with fewer bottles but higher quality, supported by increased market transparency and digital platforms.

Let’s be honest. The past three years haven’t exactly been a vintage run for fine wine investors.

Prices slid, enthusiasm cooled, and plenty of portfolios looked less like a carefully curated cellar and more like a slightly expensive lesson in timing.

But here we are in early 2026, and something interesting is happening. Not a roaring comeback. Not a champagne-popping bull run. Something quieter. More measured.

The market has stopped falling.

And in wine terms, that matters.

A market that’s stopped falling (which is progress)

After a bruising correction from 2022 to 2025, the fine wine market is now stabilising.

That might not sound thrilling, but this is often where the smart money starts paying attention. We’re seeing what analysts call “green shoots”. In simple terms, some wines are rising, others have stopped falling, and the panic sellers have largely exited.

It’s not uniform. Top-tier, blue-chip wines are leading the recovery, while mid-tier regions, particularly Burgundy, are still adjusting after some rather optimistic pricing.

Right now, the market is “bumping along the bottom”.

And while that sounds uninspiring, it’s often where the best long-term opportunities begin.

Geopolitics, chaos… and wine quietly doing its thing

Early 2026 hasn’t exactly been calm globally. Conflict in the Middle East has pushed oil prices higher and unsettled equity markets.

You’d expect all assets to feel the strain. Yet fine wine has, once again, behaved differently.

While stock markets dropped sharply, fine wine indices held steady and even edged upwards. That comes down to one of wine’s most useful traits. It doesn’t move in lockstep with equities.

With a correlation to the S&P 500 of around 0.11, wine tends to react differently when markets wobble. Not immune, but certainly less dramatic. It’s one of the reasons serious collectors continue to treat it as a long-term store of value.

Bordeaux 2016: the quiet star of the moment

If there’s a vintage quietly stealing the spotlight in 2026, it’s Bordeaux 2016.

Ten years on, it’s being reassessed and, frankly, looking rather good. This is a vintage that combines structure with freshness. Power without heaviness. The sort of balance that ages gracefully.

I’ve tasted a number of these recently, and what stands out is the energy. There’s depth, but also lift. You’re not fighting the wine. It’s composed, precise, and feels like it’s only just getting into its stride.

Critics are firmly on board, and the wines are now entering a phase where their quality is becoming more obvious in the glass. Importantly, prices haven’t run away.

That creates a rare combination. High quality, proven ageing potential, and sensible pricing.

Some standout performers are already moving. Cheval Blanc 2016 has risen strongly since late 2025, while Léoville Poyferré has shown notable upward momentum.

For anyone building a cellar with one eye on the future, this vintage is shaping up as a structural cornerstone.

Full disclosure, my own portfolio is still around 50% Bordeaux. Whether that’s good portfolio theory or just good taste is up for debate, but either way, it’s a position that continues to feel justified.

The rise of the “Super Seconds” (and why they matter)

Here’s where things get particularly interesting.

The gap between Bordeaux First Growths and the so-called “Super Seconds” has been narrowing for years. In 2026, it’s impossible to ignore.

Wines such as Pichon Lalande, Palmer, Lynch Bages, and Smith Haut Lafitte are delivering quality that often rivals the First Growths in blind tastings. Yet the pricing still sits at a meaningful discount.

In a more cautious market, buyers are focusing on value they can justify rather than prestige alone. Super Seconds offer that balance. Strong brand recognition, consistent quality, and relatively accessible entry points.

They’ve become a logical place for collectors who want quality without paying purely for legacy status.

Champagne quietly leads the recovery

While Bordeaux builds a foundation, Champagne has been getting on with things rather efficiently.

It was one of the first regions to show signs of recovery and has continued to edge upwards. The reason is straightforward. Champagne is liquid, globally recognised, and easy to trade.

It also aligns neatly with changing drinking habits. People are consuming less, but choosing better.

Prestige cuvées from houses like Krug and Dom Pérignon, along with standout growers such as Jacques Selosse and Salon, are benefiting from this shift. Demand is steady, and confidence has returned earlier than in many other regions.

Burgundy: still a tale of two markets

Burgundy, on the other hand, is having a more complicated moment.

At the very top end, the icons remain resilient. Scarcity continues to support demand for producers like DRC and Rousseau.

Below that, the picture changes. Mid-tier Burgundy surged aggressively during the boom years and hasn’t fully adjusted to current market conditions.

Prices remain high relative to demand, and liquidity is thin. Buyers are more selective, and until pricing resets further, this part of the market is likely to remain subdued.

Italy: two very different stories

Italy is splitting into two distinct camps.

On one side, Super Tuscans such as Sassicaia, Ornellaia, and Tignanello continue to perform well. They have strong global recognition, consistent quality, and reliable secondary market demand.

On the other, more traditional regions like Chianti Classico and Brunello are facing pressure. High inventory levels and reliance on the US market, combined with tariff challenges, have slowed momentum.

The result is a polarised market where the top performs strongly, while the middle struggles to find direction.

Drink less, drink better

There’s a broader shift happening beneath the surface.

Overall wine consumption is declining, particularly at the lower end of the market. But at the premium level, behaviour is changing rather than disappearing.

Consumers are buying fewer bottles, but choosing higher quality. It’s a more considered approach. Less volume, more intent.

This “drink less, but better” mindset is quietly supporting the fine wine sector, especially for producers with strong identity and craftsmanship.

A more transparent, data-driven market

The structure of the market itself is evolving as well.

Digital platforms such as Liv-ex and CultX have improved pricing transparency and access to global inventory. That’s leading to stronger participation and more consistent trading behaviour.

We’re seeing increased activity, more active bids, and a broader base of buyers returning. In simple terms, the market is becoming healthier. Less opaque, more liquid, and increasingly data-driven.

So, where does that leave us?

The fine wine market in 2026 isn’t booming, but it’s no longer falling apart either.

It’s calmer. More rational. Slightly more grown up.

Which, frankly, is no bad thing.

For collectors and investors, this phase is often where the real opportunities sit. Not in the hype, and not at the peak, but here, where prices have reset and confidence is quietly rebuilding.

If you’re selective, patient, and focused on quality, 2026 could turn out to be a rather good vintage after all.

What I’m personally buying in 2026

From a personal perspective, I’ve started to shift from concentration to diversification.

Bordeaux still forms a significant part of my holdings, but I’m increasingly allocating into Super Tuscans. Wines like Sassicaia, Ornellaia, and Tignanello offer something that’s hard to ignore right now. Global demand, strong liquidity, and consistent quality.

They behave like true “liquid assets”, and in a market that’s still finding its footing, that matters.

It’s not about abandoning Bordeaux. It’s about balance. And right now, Italy is earning a bigger seat at the table.

This article is for information purposes only and does not constitute investment advice. Always do your own research or seek professional guidance before making investment decisions.